Bayesian Optimization Tutorial 1#

Prepared by: Parisa Toofani Movaghar (ptoofani@nd.edu, 2023)

1. Introduction#

Bayesian optimization is an approach to optimize the objective function that usually takes a long time (minutes or hours) to evaluate like tuning hyperparameters of a deep neural network. Also, many optimization problems in machine learning are black-box optimization problems where the objective function is unknown (black-box function) or we have no information about its derivatives. Thanks to the Bayes theorem, such problems can be handled by developing a Bayesian optimization algorithm. There are many areas where Bayesian optimization (BO) can be a handy tool. To make an example BO has been widely used to design engineering systems (system identification) and choose laboratory experiments in materials (model selection). But this is not the only place that BO can be helpful. In computer science they are widely used in A/B testing, recommender system, robotics and reinforcement learning, environmental monitoring and sensor networks, preference learning and interactive interfaces, and tuning the hyperparameters in deep neural networks. As can be seen, BO is a class of machine-learning-based optimization algorithms that focuses on solving problems by inferring the data. But as an engineer, we should know where the best place is to use BO for our problems.

1.1. When We Need Bayesian Optimization?#

The BO algorithm works well on the problem where the input dimension is not too large. It is recommended to use this algorithm for problems with dimensions less than 20.

The objective function is continuous. We will see later that this is an assumption for the implementation of the Gaussian process (GP).

Cost matters! The function that we need to optimize is expensive to evaluate. For instance, it requires lots of iterations while our system is limited in performance (computationally cost). On the other hand, the implementation requires purchasing cloud computing environments while our budget is limited (budget limitation).

The objective function has one of the following problems: 1) the function is unknown (black box), 2) the derivatives unknown or difficult to calculate, and 3) the function is non-convex.

We are looking for the global optimum, not the local one.

1.2. Parametric vs. Nonparametric in Bayesian Optimization#

A Bayesian Optimization is an approach that uses Bayes Theorem to direct the search in order to find the minimum or maximum of an objective function. The most efficacy of the Bayesian optimization is in the black box system in which the parameter of the model is unknown (nonparametric Bayesian optimization (NBO)). But imagine that I have a beam whose characteristics are defined by stiffness, elasticity, and the applied load (more simply imagine we have a model with a, b, and c variables). Further, the goal is to find these variables in a way that the beam deflection is minimum. If we consider our model uncertain, this is another place that BO comes to help. In other words, due to the uncertainty that exists in our model, we infer our model to find the variables that describe our model well. This case is defined as the parametric Bayesian optimization (PBO).

1.2.1. Parametric Bayesian Optimization (PBO)#

In order to define the Bayesian optimization with parametric models, we consider a generic family of models parametrized by w. Imagine we have a set of data \((D)\). Since w is an unobserved quantity, we consider it as a latent random variable that has a prior distribution named \(p(w)\). Given a data D and defining the likelihood model as \(p(D|w)\), we can then infer a posterior distribution \(p(w|D)\) using the Bayes theorem.

The posterior represents the updated beliefs about the model parameters after observing the data \((D)\). The denominator correspondent with the marginal likelihood (evidence in literature) which is usually difficult to evaluate. This problem is considered a fully Bayesian approach.

1.2.2. Nonparametric Bayesian Optimization (NBO)#

The NBO is rooted in two components: 1) a Bayesian statistical model for modeling the objective function (surrogate) and 2) an acquisition function for deciding where to sample next. The mathematics here is going to be a little bit complex. We will use a space-filling experimental design to evaluate the objective function. Then we will perform the iterative calculations to allocate the remainder of a budget of N functions evaluations. Here, the surrogate model is defined as a Gaussian process (GP) that provides the Bayesian posterior probability distribution that describes the potential value for \(f(x)\) at the determined point x. Following this, the acquisition function measures the x value at the next step based on the current posterior evaluation.

2. Method#

2.1. Nonparametric Bayesian Optimization#

In this part, we will see how we can generalize the concept of PBO to NBO in order to optimize our favorite black box. This can be done by marginalizing away the weights in Bayesian linear regression and applying the kernel trick to construct a Bayesian nonparametric regression model. By kernelizing a marginalized version of Bayesian linear regression what we have already done is construct an object called a Gaussian process (GP) which we will discuss in the next part.

___________________________________________

Algorithm: Bayesian Optimization

___________________________________________

Define the search space of the objective function

Initialize the set of sampled points \(D = []\)

Specify the number of iterations \(t\)

for i = 1 to t do

Fit a Gaussian process model to the data in D

Use an acquisition function (e.g., expected improvement) to propose a new point \(x^*\)

Evaluate the objective function at \(x^*\)

Add the new point and its objective value to \(D\)

end for

Return the best-observed value in \(D\)

___________________________________________

2.2. Gaussian Process#

The Gaussian process is a nonparametric model that is characterized by its prior mean function (\(μ_0\)) and its positive definite kernel (covariance) function (\(Σ_0\)) over the function space. The interesting thing about the \(Σ_0\) is that it is constructed at each pair of points \(x_i\) and \(x_j\). Therefore, if the points \(x_i\) and \(x_j\) are close to each other in the input space, they would have a larger positive correlation which put emphasis on the belief that they have more similar function values. The prior distribution over the functions \([f(x_1 ),f(x_2 ),…,f(x_n )]\) is defined as:

Let’s go one step further and include some data in the problem. Imagine the observation is defined as \(D_n={[(x_i,f(x_i)]}_{i=1}^n\). As defined previously, the random variable \(f(x)\) conditioned on observations \(D_n\) is also normally distributed when kernelizing linear regression. Such a conditioned function is correspondent to the posterior which has the mean of \(μ_n\) and \(σ_n^2\) which is defined as follows:

Where \(Σ_0 (x,x_{1:n} )\) is a vector of covariance terms between \(x\) and \(x_{1:n}\). The posterior mean and variance evaluated at any point x represent the model prediction and uncertainty, respectively, in the objective function at the point \(x\). The posterior functions are used to select the next query point \(x_{n+1}\).

2.2.1. The prior mean function#

The prior mean function provides a possibles a possible offset. In most cases, this function is set to be a constant (\(μ(x)≡μ\)). However, when \(f\) is believed to have a trend or some application specific parametric structure, we could define the mean function to be:

Where each \(\psi_i(x)\) is a parametric function, and often a low-order polynomial in \(x\).

2.2.2. The Choice of Kernel in Gaussian Process#

One of the most important components of BO is the covariance (kernel) function which dictates the structure of the response functions that we can fit. To make an example, if we expect the response function to be periodic, we can use periodic kernels. Kernels usually are defined as the points closer in the input space that are more strongly correlated. In addition, kernels should be positive-semi definite. Different types of kernels can be defined as follows:

a) Laplacian function: this function provides a continuous and non-differentiable kernel function. In this case, if you average over your samples, you will get a straight line called Brownian bridges.

b) Power exponential or Gaussian kernel:

c) Rational Quadratic:

d) Periodic function:

e) Matern kernel: Matern kernels are a flexible class of stationary kernels. The main parameter to characterize these kernels is \(\nu>0\) which defines the smoothness. The following shows the formulation of famous Matern kernels.

# =============================================

# Importing all required libraries

# =============================================

import math

import time

import random

import matplotlib

import numpy as np

import scipy as sp

import seaborn as sns

import matplotlib.pyplot as plt

import matplotlib.gridspec as gridspec

from sklearn.gaussian_process import GaussianProcessRegressor

from mpl_toolkits.axes_grid1 import make_axes_locatable

from warnings import catch_warnings

from warnings import simplefilter

from IPython.display import Image

from matplotlib import cm

from tqdm import tqdm

# =============================================

# Creating an object-oriented model to calculate

# the various kernel functions

# =============================================

class GpKernels:

# Model initialization

def __init__(self, xa, xb, sigmaf=1, l=1):

"""

Define basic model parameters that are the same in the whole model

Inputs:

xa: sample observation (point a)

xb: sample observation (point b)

sigmaf: (model hyperparameter) vertical scale (the overall variance) -> default value = 1

l: (model hyperparameter) horizontal scale (the lengthscale) -> default value = 1

Outputs:

Nothing

"""

self.xa = xa

self.xb = xb

self.sigmaf = sigmaf

self.l = l

# Define the Laplacian function

def laplaciankernel(self):

"""

Finding the Kernel using the Laplacian function

Inputs:

self: include all model parameters in __init__ function

Outputs:

kernel values

"""

diiff = np.sqrt(sp.spatial.distance.cdist(self.xa, self.xb, 'sqeuclidean'))

sq_norm = -0.5 * np.abs(diiff) # L1 distance

return (self.sigmaf**2)*np.exp(sq_norm/(self.l**2))

# Define the power exponential or Gaussian kernel

def gausskernel(self):

"""

Finding the Kernel using the power exponential or Gaussian function

Inputs:

self: include all model parameters in __init__ function

Outputs:

kernel values

"""

sq_norm = -0.5 * sp.spatial.distance.cdist(self.xa, self.xb, 'sqeuclidean') # L2 distance (Squared Euclidian)

return (self.sigmaf**2)*np.exp(sq_norm/(self.l**2))

# Define the Rational Quadratic function

def rationalquadkernel(self, alpha):

"""

Finding the Kernel using the Rational Quadratic function

Inputs:

self: include all model parameters in __init__ function

alpha: (model hyperparameter) the scale-mixture>0

Outputs:

kernel values

"""

sq_norm = -0.5 * np.abs(np.sqrt(sp.spatial.distance.cdist(self.xa, self.xb, 'sqeuclidean')))

return (self.sigmaf**2)*np.power(np.exp(1+np.power(sq_norm, 2)/(alpha*(self.l**2))), -alpha)

# Define the Periodic function

def periodickernel(self, freq):

"""

Finding the Kernel using the Periodic function

Inputs:

self: include all model parameters in __init__ function

freq: the period or the distance between repetitions

Outputs:

kernel values

"""

diiff = np.sqrt(sp.spatial.distance.cdist(self.xa, self.xb, 'sqeuclidean'))

sq_norm = np.abs(diiff)

return (self.sigmaf**2)*np.exp(-2*np.power(np.sin(sq_norm * np.pi/freq),2)/(self.l**2))

# =============================================

# Creating an object-oriented model to implement

# the Gaussian Process model

# =============================================

class GaussianProcess:

def __init__(self, mu = None, sigma = None):

"""

Define basic model parameters that are the same in the whole model

Inputs:

mu: prior mean function

sigma: prior positive definite kernel (covariance) function

Outputs:

Nothing

"""

self.mu = mu

self.sigma = sigma

def gpprior(self, realization):

"""

Finding the samples from the prior

Inputs:

self: include all model parameters in __init__ function

realization: number of the samples to generate (number of functions to sample)

Outputs:

samples from the prior at data points

"""

return np.random.multivariate_normal(self.mu, self.sigma, realization)

def gpposterior(self, X1, y1, X2, kernel_func):

"""

Finding the posterior mean and covariance

Inputs:

self: include all model parameters in __init__ function

X1: sample observation (randomly generated)

X2: predicted points (randomly generated)

y1: sample observation values (calculated using the objective function and X1)

kernel_func: pre-defined object-oriented class (to define the kernel function)

Outputs:

muPOST: posterior mean

sigmaPOST: posterior covariance

"""

# !!! Important: here we assume that the prior mean is equal to zero

# Kernel of the noisy observations

# The kernel type is defined to be Gaussian (all other types can be used)

# Kernel between observations and observations

sigma11 = kernel_func(X1, X1).gausskernel()

# Kernel between observations and predictions

sigma12 = kernel_func(X1, X2).gausskernel()

# Kernel between predictions and predictions

sigma22 = kernel_func(X2, X2).gausskernel()

# Solve

# pos --> positive definite

solved = sp.linalg.solve(sigma11, sigma12, assume_a='pos').T

# Compute the posterior mean

muPOST = solved @ y1

# Compute the posterior covariance

sigmaPOST = sigma22 - (solved @ sigma12)

return muPOST, sigmaPOST

# =============================================

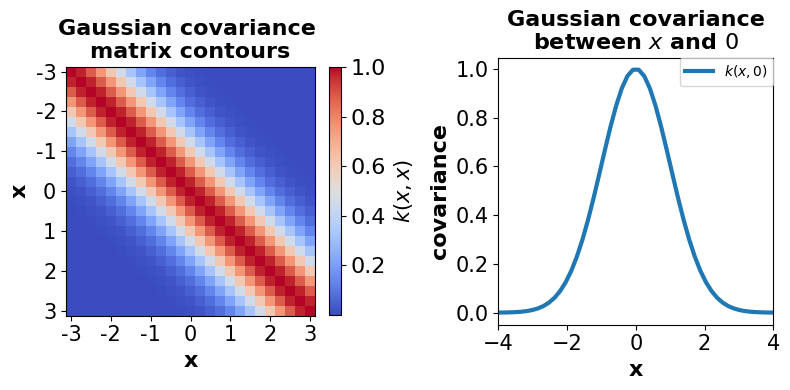

# Creating an illustration for the covariance matrix

# =============================================

# Start plotting

# The size is set to be (8,4) for capturing a better illustration

fig, (ax1, ax2) = plt.subplots(1, 2, figsize =(8,4))

# Define a limitation for x values

xlim = (-3, 3)

# Expand the shape of an array

X = np.expand_dims(np.linspace(*xlim, 25), 1)

# Define a covariance matrix using gaussian kernel

Sigma = GpKernels(X, X).gausskernel()

# Plot covariance matrix

im = ax1.imshow(Sigma, cmap=cm.coolwarm)

cbar = plt.colorbar(im, ax=ax1, fraction=0.045, pad=0.05)

# Set plots attributes

# title

ax1.set_title(('Gaussian covariance \n'

'matrix contours'), fontsize=16, fontweight = 'bold')

# labels and ticks

cbar.ax.tick_params(labelsize=16)

cbar.ax.set_ylabel(r'$k(x,x)$', fontsize=15)

ax1.set_xlabel('x', fontsize=16, fontweight='bold')

ax1.set_ylabel('x', fontsize=16, fontweight='bold')

ticks = list(range(xlim[0], xlim[1]+1))

ax1.set_xticks(np.linspace(0, len(X)-1, len(ticks)))

ax1.set_yticks(np.linspace(0, len(X)-1, len(ticks)))

ax1.set_xticklabels(ticks)

ax1.set_yticklabels(ticks)

ax1.xaxis.set_tick_params(labelsize=15)

ax1.yaxis.set_tick_params(labelsize=15)

# Grid

ax1.grid(False)

# Plot covariance with X=0 and X -> marginalizing

# Define a limitation for x values

xlim = (-4, 4)

# Expand the shape of an array

X = np.expand_dims(np.linspace(*xlim, num=50), 1)

# Define array of zero (X=0)

zero = np.array([[0]])

# Define a covariance matrix using gaussian kernel

Sigma0 = GpKernels(X, zero).gausskernel()

# Plot marginal

ax2.plot(X[:,0], Sigma0[:,0], linewidth=3, label=r'$k(x,0)$')

# Set plots attributes

# title

ax2.set_title((

'Gaussian covariance\n'

'between $x$ and $0$'), fontsize=16, fontweight = 'bold')

# labels and ticks

ax2.set_xlabel('x', fontsize=16, fontweight='bold')

ax2.set_ylabel('covariance', fontsize=16, fontweight='bold')

ax2.xaxis.set_tick_params(labelsize=15)

ax2.yaxis.set_tick_params(labelsize=15)

ax2.set_xlim(*xlim)

# legends

ax2.legend(fontsize=10,loc = 1, borderaxespad=0)

fig.tight_layout()

plt.show()

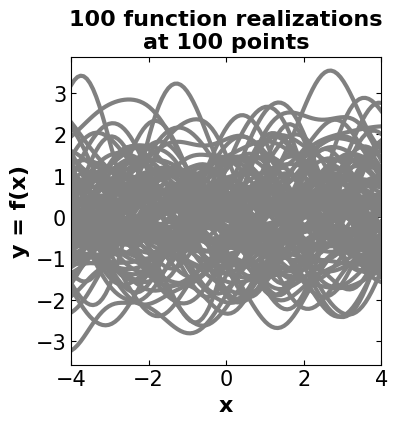

# =============================================

# Creating an illustration for drawn samples

# from the Gaussian process distribution

# =============================================

# Number of points in each function

nb_of_samples = 100

# Number of functions to sample

number_of_functions = 100

# Independent variable samples with specific limitations

# Expand the shape of an array

X = np.expand_dims(np.linspace(-4, 4, nb_of_samples), 1)

# Generate the Gaussian kernel (covariance matrix)

Σ = GpKernels(X, X).gausskernel()

# Start drawing samples from the prior

# !!! The mean is set to be zero

ys = GaussianProcess(mu=np.zeros(nb_of_samples), sigma=Σ).gpprior(number_of_functions)

# Plot the sampled functions (realizations) -> prior

# Define a plot size

priorfig = plt.figure(figsize=(4, 4))

# title

plt.title(('100 function realizations\n'

'at 100 points'), fontsize=16, fontweight = 'bold')

# generating the line plots using all iterations results

for i in range(number_of_functions):

plt.plot(X, ys[i], color = 'gray', linestyle='-', linewidth=3)

# define a and y axis labels

plt.xlabel('x', fontsize=16, fontweight='bold')

plt.ylabel('y = f(x)', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

# define a limit on xaxis

plt.xlim([-4, 4])

plt.show()

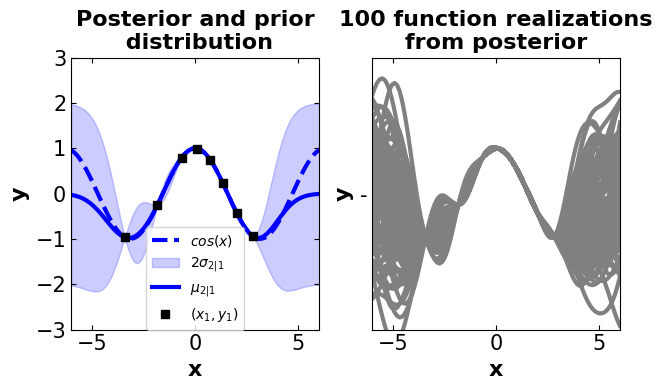

# =============================================

# Generating samples from the posterior

# =============================================

# Define the actual function (here, a periodic function (cosine) is used)

f_cos = lambda x: (np.cos(x)).flatten()

n1 = 8 # Training points (used in conditioning)

n2 = 100 # Test points in the posterior

ny = 100 # Number of functions that will be sampled from the posterior

domain = (-6, 6) # Define a specific domain

# Sample observations (randomly generated)

X1 = np.random.uniform(domain[0]+2, domain[1]-2, size=(n1, 1))

# Sample observations value (using the objective function)

y1 = f_cos(X1)

# Predicted points (randomly generated)

X2 = np.linspace(domain[0], domain[1], n2).reshape(-1, 1)

# Finding the mean and covariance of the posterior using the Gaussian process

# !!! It is important to note that prior kernel is set to be a Gaussian kernel

mu2, Sigma2 = GaussianProcess().gpposterior(X1, y1, X2, GpKernels)

# Compute the standard deviation at the test points

# -> used in defining intervals

σ2 = np.sqrt(np.diag(Sigma2))

# Randomly generated samples for posterior using

#multivariate Normal distribution

y2 = np.random.multivariate_normal(mean=mu2, cov=Sigma2, size=ny)

# =============================================

# Creating an illustration for drawn samples

# from the posterior

# =============================================

# Define a main plot size and attributes

fig2, (ax12, ax22) = plt.subplots(

nrows=1, ncols=2, figsize=(6.4, 4))

# set plot properties once so they can be easily changed later

mrk_siz = 8 # set markersize

lin_wdth = 3 # set linewidth

shade_intensity = 0.2 # set shade intensity

# title (subplot1)

ax12.set_title(('Posterior and prior\n'

' distribution'), fontsize=16, fontweight='bold')

# plot objective function (using predicted points)

ax12.plot(X2, f_cos(X2), 'b--', lw=lin_wdth, label='$cos(x)$')

#plot the intervals

ax12.fill_between(X2.flat, mu2-2*σ2, mu2+2*σ2, color='blue',

alpha=shade_intensity, label='$2 \sigma_{2|1}$')

# plot the mean

ax12.plot(X2, mu2, 'b-', lw=lin_wdth, label='$\mu_{2|1}$')

# plot the randomly generated sample points (training)

ax12.plot(X1, y1, 'ks', linewidth=mrk_siz, label='$(x_1, y_1)$')

# set label attributes

ax12.set_xlabel('x', fontsize=16, fontweight='bold')

ax12.set_ylabel('y', fontsize=16, fontweight='bold')

ax12.axis([domain[0], domain[1], -3, 3])

# adjust tick sizes

ax12.xaxis.set_tick_params(labelsize=15, direction="in",top=True, right=True)

ax12.yaxis.set_tick_params(labelsize=15, direction="in",top=True, right=True)

ax12.legend(fontsize=10,loc = 'lower center',borderaxespad=0)

# Plot samples from this function

ax22.set_title(('100 function realizations\n'

'from posterior'), fontsize=16, fontweight='bold')

# plot posterior realizations

ax22.plot(X2, y2.T, 'gray', '-', linewidth=3)

# set label attributes

ax22.set_xlabel('x', fontsize=16, fontweight='bold')

ax22.set_ylabel('y', fontsize=16, fontweight='bold')

# adjust tick sizes

ax22.xaxis.set_tick_params(labelsize=15, direction="in",top=True, right=True)

ax22.yaxis.set_tick_params(labelsize=15, direction="in",top=True, right=True)

# define domain

ax22.axis([domain[0], domain[1], -3, 3])

ax22.set_xlim([-6, 6])

# adjust subplots

plt.subplots_adjust(top = 0.92, wspace = 0.12, hspace = 0.08)

plt.tight_layout()

plt.show()

2.3. Acquisition Function#

Proposing sampling points in the search space is done by acquisition functions. They trade off exploitation and exploration. Exploitation means sampling where the surrogate model predicts a high objective and exploration means sampling at locations where the prediction uncertainty is high. Both correspond to high acquisition function values and the goal is to maximize the acquisition function to determine the next sampling point. There are two famous approaches to implementing the acquisition function named “probability of improvement (PI)” and “expected improvement (EI)”. But before getting to each algorithm let’s define what is the improvement. Imagine the objective function that we defined is \(f(x)\) and the current observe point is defined as \(x^*\), then the improvement function \(I(x)\) is defined as follows:

2.3.1. Probability of Improvement (PI)#

As we are using the GP, we know that at every point of observation, we apply a Gaussian distribution. Therefore, at point x the value of the function f(x) is sampled from the normal distribution with mean μ(x) and variance of the σ^2 (x). Finally, the probability of improvement is defined as:

# Define the function of the probability improvement

def probability_improvement(model, X, Xsamples):

"""

Finding the probability improvement

Inputs:

model: pre-defined surrogate model

X: observation data

Xsamples: randomly generated samples using random search

Outputs:

pi: probability of improvement

!!! Important note:

1- the surrogate model should be defined

using the models provided by the Scikit-learn

(like GaussianProcessRegressor), otherwise, it will not

work.

2- 1E-9 added in pi formulation is called jitter, and

it is used to avoid numerical problems.

"""

# calculate mean and stdev via surrogate function

mu, std = model.predict(Xsamples, return_std=True)

# start prediction using surrogate model

yhat = model.predict(X)

# find the best score

best = max(yhat)

# calculate the probability of improvement

pi = sp.stats.norm.cdf((mu - best) / (std+1E-9))

return pi

2.3.2. Expected Improvement (EI)#

PI only considers the probability of the point at the current step. However, the effect of the higher moments can affect the improvement (magnitude of improvement). To solve such a problem, the expected improvement is defined as follows:

# Define the function of the expected improvement

def expected_improvement(model, X, X_sample, xi=0.01):

"""

Finding the expectation of improvement

Inputs:

model: pre-defined surrogate model

X: observation data

Xsamples: randomly generated samples using random search

xi: exploitation-exploration trade-off parameter (default = 0.01)

Outputs:

ei: expectation of improvement

!!! Important note:

1- the surrogate model should be defined

using the models provided by the Scikit-learn

(like GaussianProcessRegressor), otherwise, it will not

work.

"""

# calculate mean and stdev via surrogate function

mu, sigma = model.predict(X_sample, return_std=True)

# start prediction using surrogate model

mu_sample = model.predict(X)

# find the best score

mu_sample_opt = max(mu_sample)

with np.errstate(divide='warn'):

imp = mu - mu_sample_opt - xi

Z = imp / sigma

# calculate the expectation of improvement

ei = imp * sp.stats.norm.cdf(Z) + sigma * sp.stats.norm.pdf(Z)

return ei

3. Implementing the Bayesian Optimization from scratch#

Now it is the time to put all components together, here, step by step, the Bayesian optimization is implemented using a simple function.

Here, instead of using our 1D Gaussian Process model, we will use the Gaussian process module provided by Scikit-learn.

The model that is used to be optimized is the Ackley function.

The Ackley function is a commonly used benchmark function in optimization and machine learning. It is a multimodal function that is often used to test the performance of optimization algorithms, including Bayesian optimization. The Ackley function is characterized by a large number of local minima and a relatively flat global minimum. This makes it a challenging optimization problem for many algorithms. The Ackley function is typically defined as a two-dimensional function, but it can be easily reduced to one dimension by fixing one of the input variables.

# !!! This function will be utilized later to demonstrate the convergence

# and evaluation of the Bayesian model in each step

# define a plot function to observe the function behavior per iterations

def plot_converg_iter(X_sample, Y_sample, n_init=2):

"""

Defining a plot function to observe the function behavior per iteration

Inputs:

X_sample: calculated x per iterations

Y_sample: estimated values

n_init: skip the first n_init number of samples

(initialization steps in algorithms)

Outputs:

convergence plots

"""

# Define the main figure size

plt.figure(figsize=(6.4, 4))

# Remodify samples for plotting (flattening)

x = X_sample[n_init:].ravel()

y = Y_sample[n_init:].ravel()

# define the number of iterations without initialization

r = range(1, len(x)+1)

# find the distance between points

x_neighbor_dist = [np.abs(a-b) for a, b in zip(x, x[1:])]

# create cumulative using the maximization

y_max_watermark = np.maximum.accumulate(-y)

plt.subplot(1, 2, 1)

# title

plt.title(('Distance between \n'

'consecutive x\'s'), fontsize=16, fontweight='bold')

# plot the distance between points per iteration

plt.plot(r[1:], x_neighbor_dist, 'bo-', linewidth=3, markersize=8)

# adjust labels

plt.xlabel('Iteration', fontsize=16, fontweight='bold')

plt.ylabel('Distance', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

plt.subplot(1, 2, 2)

# title

plt.title('Value of best \n'

'selected sample', fontsize=16, fontweight='bold')

# plot model evaluations per iterations

plt.plot(r, -y_max_watermark, 'ro-', linewidth=3, markersize=8)

# adjust label

plt.xlabel('Iteration', fontsize=16, fontweight='bold')

plt.ylabel('Best Y', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

plt.tight_layout()

plt.show()

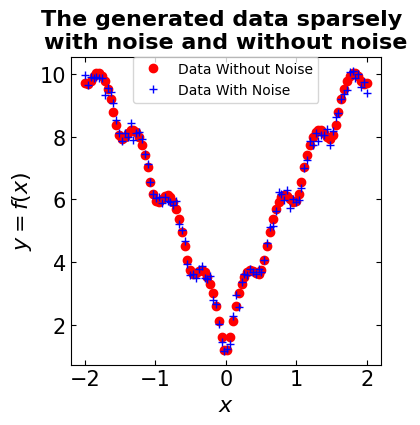

# =============================================

# Step 1: Define the objective function

# =============================================

# Define an objective function

def objectivefunction(x, noise=0.3, opt_type='Minimization'):

"""

Defining objective function

Inputs:

x: samples from a specific domain

noise: standard deviation integrated in

white noise (random Normal)

opt_type: define if the algorithm should consider the

problem as a minimization or maximization

Outputs:

objective function with/out noise (trigonometric)

"""

a = 20 # constant values

b = 0.2 # constant values

c = 2*np.pi # constant values

term1 = -a*np.exp(-b*np.sqrt(0.5*(x**2)))

term2 = -np.exp(0.5*(np.cos(c*x)))

# add noise to the model

whitenoise = np.random.normal(loc=0, scale=noise)

if opt_type == 'Minimization':

return (term1 + term2 + a + np.exp(1) + whitenoise)

else:

return -1*(term1 + term2 + a + np.exp(1) + whitenoise)

# sample the domain sparsely with noise and without noise

X_observed = np.linspace(-2, 2, 100)

y_observed = np.asarray([objectivefunction(x, noise=0.2) for x in X])

y_observed_without_noise = np.asarray([objectivefunction(x, noise=0) for x in X])

# Plot the observation

plt.figure(figsize=(4, 4))

# title

plt.title(('The generated data sparsely \n'

'with noise and without noise'), fontsize=16, fontweight='bold')

# plot data without noise

plt.plot(X_observed, y_observed_without_noise, 'ro', linewidth=8, label='Data Without Noise')

# plot data with noise

plt.plot(X_observed, y_observed, 'b+', linewidth=8, label='Data With Noise')

# define labels attributes

plt.xlabel('$x$', fontsize=16, fontweight='bold')

plt.ylabel('$y = f(x)$', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

# adjust legends

plt.legend(fontsize=10,borderaxespad=0)

plt.show()

# =============================================

# Import model-specific libraries (from Scikit-learn)

# =============================================

from sklearn.gaussian_process import GaussianProcessRegressor

from sklearn.gaussian_process.kernels import ConstantKernel, Matern

# =============================================

# Step 2: Define the Gaussian process model

# =============================================

"""

Models description:

-----------------------------------

Src: https://scikit-learn.org/stable/modules/generated/sklearn.gaussian_process.GaussianProcessRegressor.html

GaussianProcessRegressor:

1- kernel: kernel instance, default=None

2- alpha: float or ndarray of shape (n_samples,), default=1e-10

-----------------------------------

Src: https://scikit-learn.org/stable/modules/generated/sklearn.gaussian_process.kernels.ConstantKernel.html

ConstantKernel:

constant_value: float, default=1.0

-----------------------------------

Src: https://scikit-learn.org/stable/modules/generated/sklearn.gaussian_process.kernels.Matern.html

Matern:

length_scale: float or ndarray of shape (n_features,), default=1.0

nu: float, default=1.5

The parameter nu controls the smoothness of the learned function.

"""

# initialize the model

# define specific X and y values for custom Bayesian model

#----------------------------------------------------------------------------

# !!! for solving the Bayesian model (using custom function) we need to inverse

# the problem and turn it to maximization to be able to catch the global optimal point

#----------------------------------------------------------------------------

X_bo_custom = np.linspace(-2, 2, 5)

y_bo_custom = -np.asarray([objectivefunction(x, noise=0.2) for x in X_bo_custom])

# reshape into rows and cols

X_bo_custom = X_bo_custom.reshape(len(X_bo_custom), 1)

y_bo_custom = y_bo_custom.reshape(len(y_bo_custom), 1)

noise=0.2

m52 = ConstantKernel(1.0) * Matern(length_scale=1.0, nu=2.5)

gpr_bo = GaussianProcessRegressor(kernel=m52, alpha=noise**2)

# fit the model

gpr_bo.fit(X_bo_custom, y_bo_custom)

GaussianProcessRegressor(alpha=0.04000000000000001,

kernel=1**2 * Matern(length_scale=1, nu=2.5))In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

GaussianProcessRegressor(alpha=0.04000000000000001,

kernel=1**2 * Matern(length_scale=1, nu=2.5))# =============================================

# Step 3: Perform the optimization process

# =============================================

# Defining the optimization for acquisition function

def opt_acquisition(Xsamples, X, y, surrogate, algorithm):

"""

Defining the optimization for acquisition function

Inputs:

Xsamples: generated samples per iteration

X: observed samples

y: observed samples values

surrogate: surrogate model (Gaussian process)

algorithm: probability improvement or expectation improvement

Outputs:

the sample corresponds to the best score

"""

# calculate the acquisition function

scores = algorithm(surrogate, X, Xsamples)

# find the index of best score

ix = np.argmax(scores)

return Xsamples[ix, 0]

# Add timer to catch the calculation runtime

t1 = time.time()

# Define lists to capture the output of the model

f_actual = [] # actual values of the model

estimated_values = [] # estimated values using Gaussian process

x_per_iteration = [] # calculated x per iterations

# start an iteration

for i in tqdm(range(100)):

# generate samples

X_samples_bo = np.random.random(100)

# reshape samples to get the exact dimension

X_samples_bo = X_samples_bo.reshape(len(X_samples_bo), 1)

# select the next point to sample

x = opt_acquisition(X_samples_bo, X_bo_custom, y_bo_custom, gpr_bo, expected_improvement)

# sample the point

actual = objectivefunction(x, opt_type='Maximization')

# summarize the finding

est, _ = gpr_bo.predict([[x]], return_std=True)

f_actual.append(actual)

estimated_values.append(est)

x_per_iteration.append(x)

# add the data to the dataset

X_bo_custom = np.vstack((X_bo_custom, [[x]]))

y_bo_custom = np.vstack((y_bo_custom, [[actual]]))

# update the model

gpr_bo.fit(X_bo_custom, y_bo_custom)

t2 = time.time()

print("Run time is: ", t2-t1)

100%|██████████| 100/100 [00:05<00:00, 17.33it/s]

Run time is: 5.780000925064087

# =============================================

# Step 4: Demonstrate the calculated results

# =============================================

# Find the index of the best-calculated value

ix = np.argmax(y_bo_custom)

print("============================================\n")

print("The optimal point is: ", X_bo_custom[ix][0])

print("============================================\n")

# As we inverse the problem (turn minimization to maximization)

# it is necessary to multiply the model evaluations by -1

print("The optimal value is: ", -y_bo_custom[ix][0])

print("============================================\n")

print("Run time is: %s" %(t2-t1))

print("============================================\n")

============================================

The optimal point is: 0.006255250376929866

============================================

The optimal value is: 0.29083370411817233

============================================

Run time is: 5.780000925064087

============================================

# =============================================

# Step 5: Demonstrate the convergence plots

# =============================================

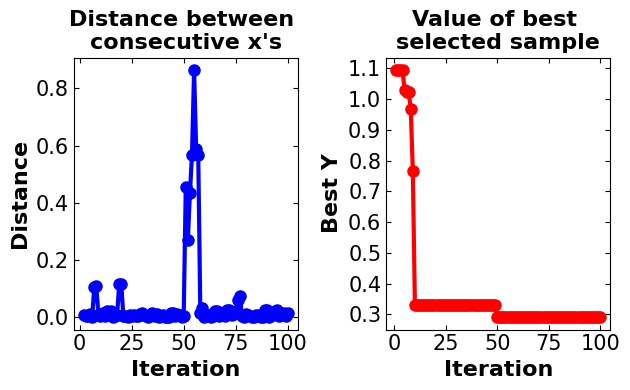

plot_converg_iter(np.array(X_bo_custom), np.array(-y_bo_custom), n_init=5)

Discussion:#

In the custom model generated Bayesian optimization, the number of iterations is set to 100, and in each iteration, 100 random samples are generated. The expected improvement is defined as an algorithm for the acquisition function. It is important to note that 5 samples are generated to initialize the algorithm. As this algorithm is developed to solve the maximization problem the objective function for maximization is utilized. The run time for performing the algorithm is approximately between 2.5 to 6s which is extremely good and it makes the algorithm efficient. The global optimum is captured by the algorithm between the points of (0.002, 0.06) and (0.007, 0.4) which is near the actual global optimum. Also, it is worth mentioning that the algorithm converges to the optimal point after approximately 25 iterations.

!!! The algorithm is based on randomly generated samples. Therefore, after running the Notebook, you may get different results.

4. Libraries to Perform Bayesian Optimization#

4.1. GpyOpt#

GPyOpt is a Python open-source library for Bayesian Optimization developed by the Machine Learning group of the University of Sheffield. It is based on GPy, a Python framework for Gaussian process modeling. GpyOpt is able to automatically configure the models and Machine Learning algorithms and design the wet-lab experiments while saving time and money. Among other functionalities, GPyOpt can design experiments in parallel, use cost models and mix different types of variables in system designs.

# =============================================

# Import model-specific libraries

# =============================================

import GPy

import GPyOpt

from GPyOpt.methods import BayesianOptimization

"""

Models description:

-----------------------------------

Src: https://gpyopt.readthedocs.io/en/latest/GPyOpt.methods.html

BayesianOptimization: main class to initialize a Bayesian Optimization method

1- f: function to optimize

2- domain: list of dictionaries containing the description of the inputs variables

3- Initial_design_numdata: number of initial points that are collected jointly

before start running the optimization

4- Acquisition_type: type of acquisition function to use. - ‘EI’, expected improvement. -

‘EI_MCMC’, integrated expected improvement (requires GP_MCMC model). -

‘MPI’, maximum probability of improvement. -

‘MPI_MCMC’, maximum probability of improvement (requires GP_MCMC model). -

‘LCB’, GP-Lower confidence bound. -

‘LCB_MCMC’, integrated GP-Lower confidence bound (requires GP_MCMC model).

"""

# start to capture the time (for runtime calculation)

t3 = time.time()

# define domain characteristics

bds = [{'name': 'X', 'type': 'continuous', 'domain': (-2, 2)}]

# start optimization using GpyOpt

# !!! the acquisition function and initial number of

# points defined the same as the custom-developed BO model

# create model

gpy_bo = BayesianOptimization(f=objectivefunction,

domain=bds,

acquisition_type ='EI',

initial_design_numdata=5)

# run the model

gpy_bo.run_optimization(max_iter=100)

t4 = time.time()

# calculate the runtime

Runtime = t4 - t3

print("============================================\n")

# Get the optimal point using x_opt attribute

print("The optimal point is: ", gpy_bo.x_opt[0])

print("============================================\n")

# Get the optimal value using fx_opt attribute

print("The optimal value is: ", gpy_bo.fx_opt)

print("============================================\n")

# Report the runtime

print("Run time is: ", Runtime)

print("============================================\n")

============================================

The optimal point is: -0.003514669698889943

============================================

The optimal value is: 0.4876386286568032

============================================

Run time is: 55.83359694480896

============================================

# Demonstrate the convergence plots

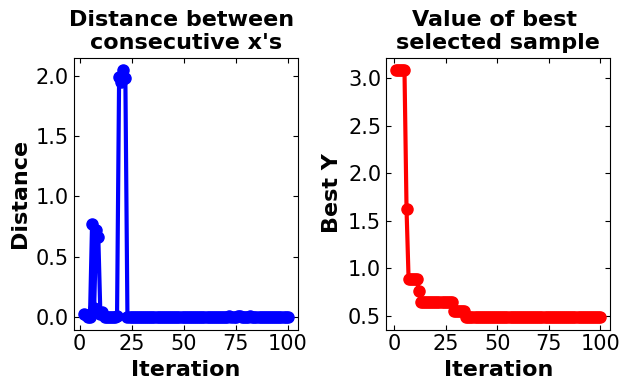

plot_converg_iter(gpy_bo.X, gpy_bo.Y, n_init=5)

Discussion#

In the GpyOpt, all model characteristics are set to be the same as the BO custom model to make them comparable. As can be seen, the algorithm takes more steps until converging to the optimal point (more than 60 iterations). Also, when the model gets near the optimal point experiences a smaller distance. The interesting point about this model is the large runtime which makes it inefficient for such a simple model.

4.2. Scikit-Optimize#

Scikit-optimize is a library for sequential model-based optimization that is based on Scikit-learn. It also supports Bayesian optimization using Gaussian processes. The API is designed around minimization, hence, we have to provide negative objective function values.

# =============================================

# Import model-specific libraries

# =============================================

from skopt import gp_minimize

"""

Models description:

-----------------------------------

Src: https://scikit-optimize.github.io/stable/modules/generated/skopt.gp_minimize.html#skopt.gp_minimize

BayesianOptimization: Bayesian optimization using Gaussian Processes.

1- func: callable, Function to minimize. Should take a single list of parameters and return the objective value.

2- n_calls: int, default: 100, Number of calls to func.

3- n_random_starts: int, default: None, Number of evaluations of func with random points before

approximating it with base_estimator.

4- acq_func: string, default: "gp_hedge", Function to minimize over the gaussian prior. Can be either:

"LCB" for lower confidence bound.

"EI" for negative expected improvement.

"PI" for negative probability of improvement.

"gp_hedge" Probabilistically choose one of the above three acquisition

functions at every iteration.

"EIps" for negated expected improvement per second to take into account

the function compute time. Then, the objective function is assumed to return two values,

the first being the objective value and the second being the time taken in seconds.

"PIps" for negated probability of improvement per second. The return type of

the objective function is assumed to be similar to that of "EIps"

5- noise: float, default: “gaussian”. Use noise=”gaussian” if the objective returns noisy observations.

The noise of each observation is assumed to be iid with mean zero and a fixed variance.

If the variance is known before-hand, this can be set directly to the variance of the noise.

Set this to a value close to zero (1e-10) if the function is noise-free.

Setting to zero might cause stability issues.

"""

# start to capture the time (for runtime calculation)

t5 = time.time()

# start optimization using ScikitOpt

# !!! the acquisition function and initial number of

# points defined same as the custom developed BO model

# create and run the model

skopt_bo = gp_minimize(lambda x: objectivefunction(np.array(x))[0], # the function to minimize

[(-2, 2)], # the bounds on each dimension of x

acq_func="EI", # the acquisition function

n_calls=100, # the number of evaluations of f

n_random_starts=5, # the number of random initialization points

noise=0.1**2,) # the noise level (optional)

t6 = time.time()

# calculate the runtime

Runtime1 = t6 - t5

print("============================================\n")

# Get the optimal point using x[0] attribute

print("The optimal point is: ", skopt_bo.x[0])

print("============================================\n")

# Get the optimal value using fun attribute

print("The optimal value is: ", skopt_bo.fun)

print("============================================\n")

# Report the runtime

print("Run time is: ", Runtime1)

print("============================================\n")

============================================

The optimal point is: 0

============================================

The optimal value is: 0.2715006871998069

============================================

Run time is: 32.40369367599487

============================================

# Demonstrate the convergence plots

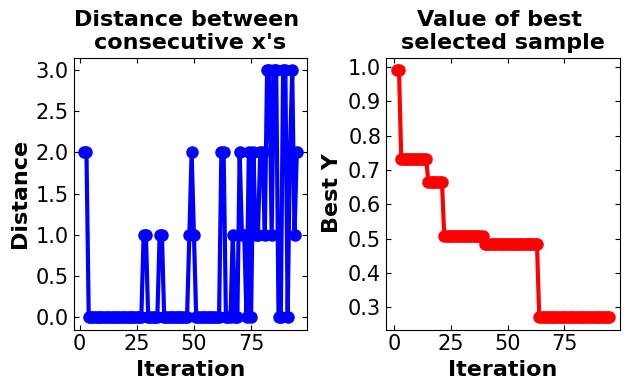

plot_converg_iter(np.array(skopt_bo.x_iters), np.array(skopt_bo.func_vals), n_init = 5)

Discussion#

Same as GpyOpt, in the ScikitOpt model all parameters are set to be the same as the custom BO model to make it comparable. In the ScikiOpt, the model converges fast to the optimal point (in less than 25 iterations) and after 75 iterations, there is a minor change in the model results. The algorithm is also available to capture the global optimum with approximately good accuracy. After 25 iterations, oscillation is detected in model distances. The runtime of this model is also high in comparison with the custom-generated model.

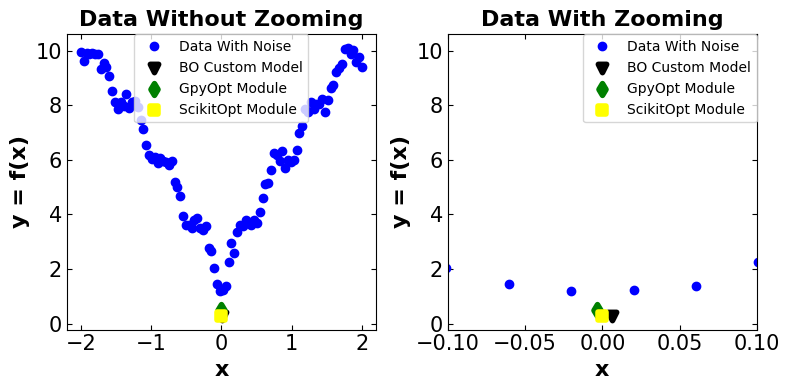

4.3. Comparison Between the Results of the Custom BO Model, GpyOPT, and Scikit-Opt#

# =============================================

# Providing a plot to compare BO custom model

# with the results of the commercial

# package models

# =============================================

# Plot the observation

fig_compare = plt.figure(figsize=(8, 4))

plt.subplot(1, 2, 1)

# title

plt.title(('Data Without Zooming'), fontsize=16, fontweight='bold')

# plot data with noise

plt.plot(X_observed, y_observed, 'bo', linewidth=8, label='Data With Noise')

# plt.scatter(X_bo_custom, -y_bo_custom_predict, c='r')

plt.scatter(X_bo_custom[ix], -y_bo_custom[ix], marker = 'v', c = 'k', linewidth=4, label='BO Custom Model')

plt.scatter(gpy_bo.x_opt[0], gpy_bo.fx_opt, marker = 'd', c = 'g', linewidth=4, label='GpyOpt Module')

plt.scatter(skopt_bo.x[0], skopt_bo.fun, marker = 's', c = 'yellow', linewidth=4, label='ScikitOpt Module')

# define labels attributes

plt.xlabel('x', fontsize=16, fontweight='bold')

plt.ylabel('y = f(x)', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

# adjust legends

plt.legend(fontsize=10, loc='upper center', borderaxespad=0)

plt.subplot(1, 2, 2)

# title

plt.title(('Data With Zooming'), fontsize=16, fontweight='bold')

# plot data with noise

plt.plot(X_observed, y_observed, 'bo', linewidth=8, label='Data With Noise')

# plt.scatter(X_bo_custom, -y_bo_custom_predict, c='r')

plt.scatter(X_bo_custom[ix], -y_bo_custom[ix], marker = 'v', c = 'k', linewidth=4, label='BO Custom Model')

plt.scatter(gpy_bo.x_opt[0], gpy_bo.fx_opt, marker = 'd', c = 'g', linewidth=4, label='GpyOpt Module')

plt.scatter(skopt_bo.x[0], skopt_bo.fun, marker = 's', c = 'yellow', linewidth=4, label='ScikitOpt Module')

# define labels attributes

plt.xlabel('x', fontsize=16, fontweight='bold')

plt.ylabel('y = f(x)', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

plt.xlim([-0.1, 0.1])

# adjust legends

plt.legend(fontsize=10,borderaxespad=0)

plt.tight_layout()

plt.show()

Approach |

Optimal Point |

Optimal Value |

Run Time (s) |

|---|---|---|---|

Custom BO Model |

~0.0062 |

~0.2908 |

~5.7800 |

GpyOpt |

~-0.0035 |

~0.4876 |

~55.8335 |

Scikit-Opt |

~0.0000 |

~0.2710 |

~32.4036 |

Discussion:#

!!! It is important to note that the estimated results can differ by each time running this Jupyter Notebook. Therefore, the sign “~” has been put beside the results. Also, there should not be a major discrepancy between the results each time running the Jupyter Notebook.

Main Observation Optimal Point: (0, 1.1772)

Comparing the results between three different algorithms and the main model all algorithms get close to the optimal point with some discrepancies. The existence of discrepancy considering the noisy model with lots of local optimum points is reasonable. Considering that all algorithms perform somehow well in capturing the optimal point, the parameter that differentiates between these three algorithms could be the model run time. The custom-generated BO model performs well by having a run time of 5.7800s. After that, Scikit-Opt and GpyOpt have second and third places, respectively. The first reason is that the custom-generated model skips lots of error-checking steps provided by other packages. This does not guarantee that the BO model performs well on other problems with more complex space or higher dimensions.

5. Advanced Usage of Bayesian Optimization#

5.1. Hyper-Parameter Tuning#

Hyperparameter-tuning is the process of searching the most accurate hyperparameters for a dataset with a Machine Learning algorithm. To do this, we fit and evaluate the model by changing the hyperparameters one by one repeatedly until we find the best accuracy.

What is the difference between a parameter and a hyperparameter?

Model parameters: These are the parameters that are estimated by the model from the given data. For example the weights of a deep neural network.

Model hyperparameters: These are the parameters that cannot be estimated by the model from the given data. These parameters are used to estimate the model parameters. For example, the learning rate in deep neural networks.

But the main question is that what is the efficient approach for tuning the hyper-parameters?

In general, there are four main approaches including:

Manual Search

Grid Search CV

Random Search CV

Bayesian Optimization

5.1.1 Manual Search#

Manual hyperparameter tuning involves experimenting with different sets of hyperparameters manually i.e. each trial with a set of hyperparameters will be performed by you. This technique will require a robust experiment tracker which could track a variety of variables from images, and logs to system metrics.

5.1.2 Grid Search#

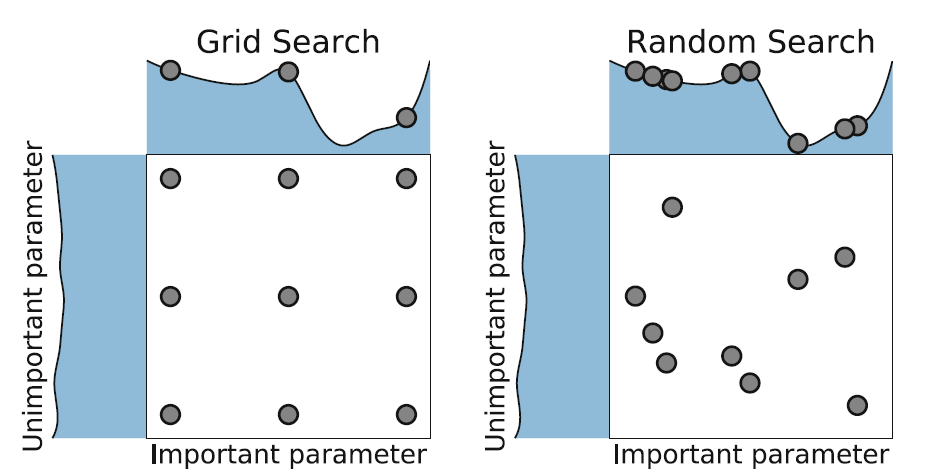

In the grid search method, we create a grid of possible values for hyperparameters. Each iteration tries a combination of hyperparameters in a specific order. It fits the model on every combination of hyperparameters possible and records the model performance. Finally, it returns the best model with the best hyperparameters.

5.1.3 Random Search#

In the random search method, we create a grid of possible values for hyperparameters. Each iteration tries a random combination of hyperparameters from this grid, records the performance, and lastly returns the combination of hyperparameters that provided the best performance.

Image Source: Elyse Lee (2019), An Intro to Hyper-parameter Optimization using Grid Search and Random Search, Medium.com. url

5.1.4 Bayesian Optimization#

In the case of Hyper-Parameter tuning, there are lots of machine learning algorithms (our black-box problems) such as Descision-Trees, random forests, extreme gradient boosting (XGBoost), and deep neural networks which comprise lots of different types of Hyper-Parameters. Tuning such parameters can extremely impact the performance of the whole model. Some algorithms such as XGBoost (the one that is used in the further problem) and DNNs have many Hyper-Parameters that make the process of optimizing them a challenging task.

The Hyper-Parameter optimization problem can be defined as:

where \(\Phi\) is the Hyper-Parameter response function, \(\gamma\) defines the Hyper-Parameters, \(\Delta\) is a search space, and \({\gamma^{(1)}, ..., \gamma^{(S)}}\) represents the trial points.

Hence, Hyper-Parameter optimization is defined as the minimization of \(\Phi (\gamma)\) over \(\gamma \in \Delta\).

As can be seen, the problem is the same as the one we had in the \(1D\) BO approach. So, the problem can be solved using the following steps:

Define a prior measure such as Gaussian Process (GP)

Getting the posterior measure given some observation over the objective function by combining the likelihood and prior

Finding the next step using the loss function

However, solving such a problem is not an easy task for coding from scratch. For this reason, several developers have developed modules like HyperOpt, GpyOpt, and ScikitOpt to solve these problems.

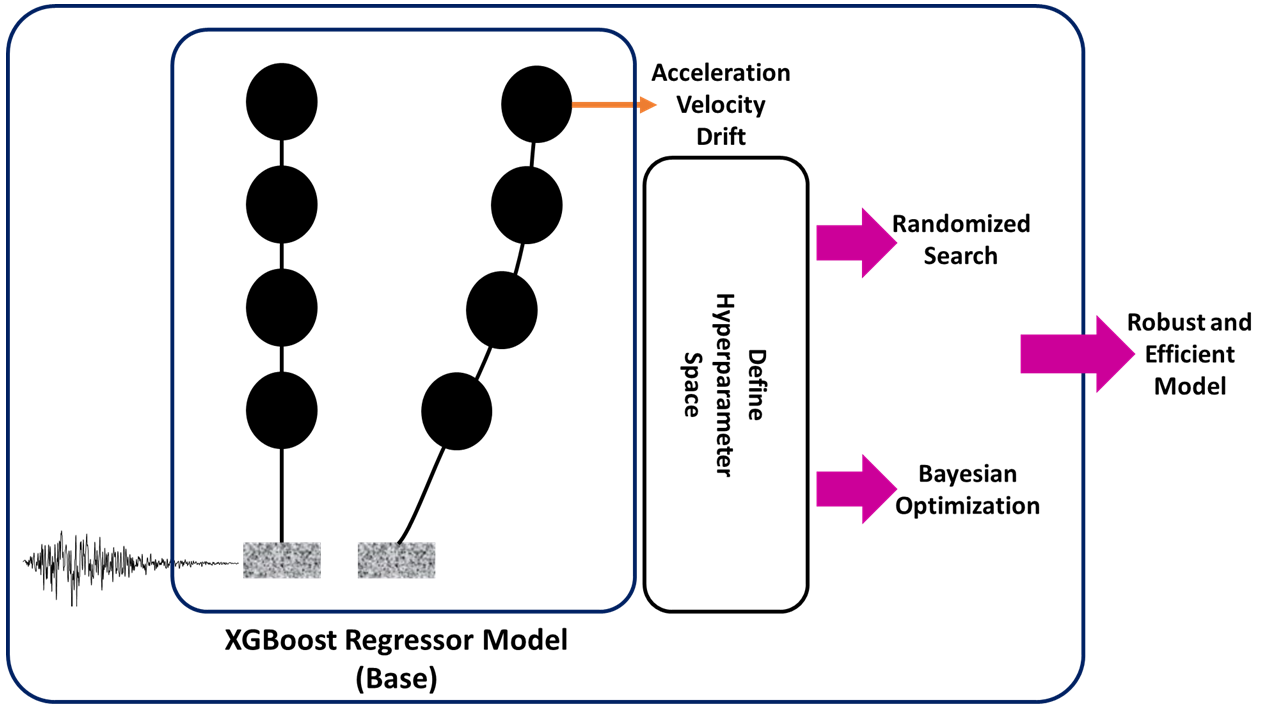

5.1.5 Real-World Problem: Tuning HyperParameter in ML-Based Building Response Estimation Model Under an Earthquake#

Problem Definition:

A multi-degree of freedom (MDOF) simplified 2D shear-building model combined with 222 ground motions ranging from 0.05g to 1.80 g peak ground accelerations are analyzed using OpenSeesPy. The nonlinearity of models is created using the inter-story hysteretic model proposed in HAZUS. methodology, considering the building type, number of stories, and construction year. Then, response-history analysis is conducted to generate a comprehensive dataset for machine learning algorithms. The proposed algorithm used ground motion as well as structural characteristics such as PGA, Sa (0.2s), Sa(1s), and Sa(T1), story height, story mass, and period as input variables to estimate the responses of different structures.

By performing several analyses, the XGboost Regression model performs better on the mentioned model. However, we still looking for improving the generated model using the hyperparameter tuning approaches.

Goal: We are interested to perform both Random Search and Bayesian Optimization to find optimal Hyperparameters of the model.

Step 1: Import required libraries#

The first and foremost step to solving this question is importing the required libraries. For this specific problem, we require a Randomized search and cross-validation (provided by sci-kit learn), and XGBoost regressor library.

# =============================================

# Importing all required libraries

# =============================================

import pandas as pd # Dataframe management

from scipy.stats import uniform # random data generation using Unifrom distribution

from xgboost import XGBRegressor # XGboost Resgressor for performing regression analysis and predicting model

from sklearn.preprocessing import MinMaxScaler # It is used to normalize data based on the minimum and maximum

from sklearn.model_selection import RandomizedSearchCV, cross_val_score # Baseline and model selection algorithm

Step 2: Prepare the dataset#

The dataset is provided on the GitHub repository and it can be imported using the following links. The data also can get extracted using the Pandas module.

It is important to note that there are several inputs that do not have any effect on the prediction model, therefore they are removed from the dataset (Data Cleaning).

# =============================================

# Download the dataset

# =============================================

# Get the raw data from Github and extract its data using Pandas dataframe (read_csv) method

dataset = pd.read_csv("https://raw.githubusercontent.com/ParisaToofani/OptimizationJourney/main/OptimizationinDL/c2.csv")

# The mentioned columns are dropped from dataset for two reasons:

# 1. They do not have critical effect on the model and data

# 2. Reduce the dimensionality of the model

dataset=dataset.drop(['#', 'seismicity', 'story_num', 'disp_dir1', 'react_dir1', 'Mass', 'Period', 'accel_dir1', 'disp_dir1', 'vel_dir1'], axis=1)

# In order to show the dataset we only need to call it down

dataset

| sa02 | sa1 | sat | pga | zi/h | Total height | drift_dir1 | |

|---|---|---|---|---|---|---|---|

| 0 | 1.9294 | 0.7536 | 2.1144 | 0.5831 | 0.0 | 3.2 | 0.000000 |

| 1 | 0.2842 | 0.2023 | 0.2172 | 0.1395 | 0.0 | 3.2 | 0.000000 |

| 2 | 0.3191 | 0.3029 | 0.3062 | 0.1591 | 0.0 | 3.2 | 0.000000 |

| 3 | 0.8270 | 0.3352 | 1.0861 | 0.3378 | 0.0 | 3.2 | 0.000000 |

| 4 | 0.8847 | 0.3805 | 1.2538 | 0.5465 | 0.0 | 3.2 | 0.000000 |

| ... | ... | ... | ... | ... | ... | ... | ... |

| 19975 | 0.7142 | 0.5385 | 0.5041 | 0.3854 | 1.0 | 38.4 | 0.005181 |

| 19976 | 0.6358 | 0.4857 | 0.3770 | 0.3461 | 1.0 | 38.4 | 0.001399 |

| 19977 | 0.9575 | 0.2976 | 0.2387 | 0.4431 | 1.0 | 38.4 | 0.007332 |

| 19978 | 0.4173 | 0.1540 | 0.1221 | 0.1727 | 1.0 | 38.4 | 0.001016 |

| 19979 | 0.5971 | 0.2945 | 0.2631 | 0.3138 | 1.0 | 38.4 | 0.008683 |

19980 rows × 7 columns

Step 3: Define a model#

Here, the XGBoost model is utilized for performing the machine learning algorithm. The reason for utilizing such an algorithm is that XGBoost usually performs well on large-scale machine-learning problems on structured datasets. The second reason is that this algorithm can provide good accuracy compared to neural network approaches.

The main Hyper-Parameters of the XGBoost model for the regression task are:

\(\eta\) (Learning Rate): Step size shrinkage used in the update to prevent overfitting. After each boosting step, we can directly get the weights of new features, and \(\eta\) shrinks the feature weights to make the boosting process more conservative. The default value is 0.3 and accepts values between \([0, 1]\).

\(\gamma\): Minimum loss reduction required to make a further partition on a leaf node of the tree. The larger \(\gamma\) is, the more conservative the algorithm will be. The default value is 0.0 and accepts values between \((0, \infty]\).

Maximum depth: It defines the maximum depth of a tree. Increasing this value will make the model more complex and more likely to overfit. 0 indicates no limit on depth. Beware that XGBoost aggressively consumes memory when training a deep tree. The default value is 6.0 and accepts values between \([0, \infty]\).

Min-chile-weight: Minimum sum of instance weight (hessian) needed in a child. If the tree partition step results in a leaf node with the sum of instance weight less than min_child_weight, then the building process will give up further partitioning. In a linear regression task, this simply corresponds to a minimum number of instances needed to be in each node. The larger min_child_weight is, the more conservative the algorithm will be. The default value is 6.0 and accepts values between \([0, \infty]\).

n_estimators: The number of trees (or rounds) in an XGBoost model is specified to the XGBClassifier or XGBRegressor class in the n_estimators argument. The default in the XGBoost library is 100.

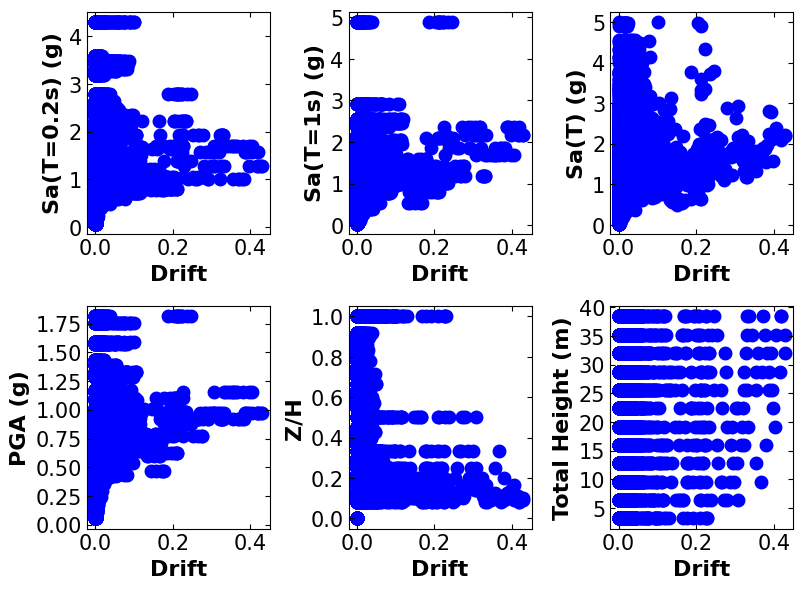

Step 4: Data visualization#

Before performing any machine learning task, it is important to have some visualization regarding the data. This can help to decide on various things like normalization, data extraction, and the best algorithm.

# =============================================

# Visualizing model output regarding each model

# feature

# =============================================

# Plot the observation

# The standard plot size get modified to capture better visualization

fig_compare = plt.figure(figsize=(8, 6))

plt.subplot(2, 3, 1)

# plot data with respect to the Sa02

plt.scatter(dataset['drift_dir1'], dataset['sa02'], marker = 'o', c = 'b', linewidth=4)

# define labels attributes

plt.xlabel('Drift', fontsize=16, fontweight='bold')

plt.ylabel('Sa(T=0.2s) (g)', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

#------------------------------------------------------------------------------------

plt.subplot(2, 3, 2)

# plot data with respect to the Sa01

plt.scatter(dataset['drift_dir1'], dataset['sa1'], marker = 'o', c = 'b', linewidth=4)

# define labels attributes

plt.xlabel('Drift', fontsize=16, fontweight='bold')

plt.ylabel('Sa(T=1s) (g)', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

#------------------------------------------------------------------------------------

plt.subplot(2, 3, 3)

# plot data with respect to the Sa0t

plt.scatter(dataset['drift_dir1'], dataset['sat'], marker = 'o', c = 'b', linewidth=4)

# define labels attributes

plt.xlabel('Drift', fontsize=16, fontweight='bold')

plt.ylabel('Sa(T) (g)', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

#------------------------------------------------------------------------------------

plt.subplot(2, 3, 4)

# plot data with respect to the pga

plt.scatter(dataset['drift_dir1'], dataset['pga'], marker = 'o', c = 'b', linewidth=4)

# define labels attributes

plt.xlabel('Drift', fontsize=16, fontweight='bold')

plt.ylabel('PGA (g)', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

#------------------------------------------------------------------------------------

plt.subplot(2, 3, 5)

# plot data with respect to the zi/h

plt.scatter(dataset['drift_dir1'], dataset['zi/h'], marker = 'o', c = 'b', linewidth=4)

# define labels attributes

plt.xlabel('Drift', fontsize=16, fontweight='bold')

plt.ylabel('Z/H', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

#------------------------------------------------------------------------------------

plt.subplot(2, 3, 6)

# plot data with respect to the Total height

plt.scatter(dataset['drift_dir1'], dataset['Total height'], marker = 'o', c = 'b', linewidth=4)

# define labels attributes

plt.xlabel('Drift', fontsize=16, fontweight='bold')

plt.ylabel('Total Height (m)', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

plt.tight_layout()

plt.show()

Step 5: Preparing Data#

# =============================================

# Preparing data

# =============================================

# Create an array of data for better data extraction

data = dataset.iloc[:, :].values

# Get the model input (the first 6 columns)

Xdata=data[:,:6]

# Get the model output (the last column)

ydata=data[:,6:]

# Normalizing data based on the minimum and maximum values

scaler_x = MinMaxScaler()

scaler_y = MinMaxScaler()

# Fitting data to scalar (inputs)

print(scaler_x.fit(Xdata))

# Transform data the get the scaled data

xscale=scaler_x.transform(Xdata)

# Fitting data to scalar (output)

print(scaler_y.fit(ydata))

# Transform data the get the scaled data

yscale=scaler_y.transform(ydata)

MinMaxScaler()

MinMaxScaler()

# =============================================

# Splitting the data

# =============================================

# !!! This is a necessary step to help us with prediction model evaluation

# 85% of data are used for model training and 15% of

# data are used for further steps (model evaluation)

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(xscale, yscale, test_size = 0.15, random_state = 0)

Step 6: Defining the baseline model#

In this step, the XGBRegressor is utilized to create a model. It is important to note that the model is developed based on the default parameters. Also, the evaluation model here (the baseline) is defined based on the mean of the cross-validation score. The scoring parameter is also chosen as a negative mean squared error.

Here, a brief discussion is provided about the cross-validation score based on an article by Stephen Allwright.

Cross_val_score is a function in the Scikit-Learn package which trains and tests a model over multiple folds of your dataset. This cross-validation method gives you a better understanding of model performance over the whole dataset instead of just a single train/test split. Cross_val_score is used as a simple cross-validation technique to prevent over-fitting and promote model generalization. The process that cross_val_score uses is typical for cross-validation and follows these steps:

The number of folds is defined, by default, this is 5

The dataset is split up according to these folds, where each fold has a unique set of testing data

A model is trained and tested for each fold

Each fold returns a metric for its test data

The mean and standard deviation of these metrics can then be calculated to provide a single metric for the process

# =============================================

# Instantiate an XGBRegressor with default

# hyperparameter settings

# =============================================

xgb = XGBRegressor()

# compute a baseline

baseline = cross_val_score(xgb, X_train, y_train, scoring='neg_mean_squared_error').mean()

Step 7: Tuning Hyper-Parameters#

In this step, we define a dictionary of Hyper-Parameters and their correspondent range (param-dist), or the list of dictionaries (bds) to utilize them in both random search and the “BayesianOptimization” model.

# =============================================

# Hyper-parameter tuning using randomized search

# model

# =============================================

# Define the model hyperparameters and the range

# to be tuned

param_dist = {"learning_rate": uniform(0, 1),

"gamma": uniform(0, 5),

"max_depth": range(1,50),

"n_estimators": range(1,300),

"min_child_weight": range(1,10)}

# Perform random search task for 25 iterations

# Model data:

# Src: https://scikit-learn.org/stable/modules/generated/sklearn.model_selection.RandomizedSearchCV.html

# xgb: XGBoost regression model used for training data

# param_distributions: model hyper-parameters

# scoring: model evaluation metric

# n_iter: number of iterations

rs = RandomizedSearchCV(xgb, param_distributions=param_dist,

scoring='neg_mean_squared_error', n_iter=25)

# Fitting the model structure to perform-

# hyper-parameter tuning

rs.fit(X_train, y_train);

# =============================================

# Model structure and parameters value after

# performing Hyper-Parameter tuning

# =============================================

print("============================================\n")

print("The optimal learning rate is: ", 0.3195)

print("============================================\n")

print("The optimal gamma is: ", 0.4097)

print("============================================\n")

print("The optimal max_depth is: ", 20)

print("============================================\n")

print("The optimal n_estimators is: ", 101)

print("============================================\n")

print("The optimal min_child_weight is: ", 7)

print("============================================\n")

rs.best_estimator_

============================================

The optimal learning rate is: 0.3195

============================================

The optimal gamma is: 0.4097

============================================

The optimal max_depth is: 20

============================================

The optimal n_estimators is: 101

============================================

The optimal min_child_weight is: 7

============================================

XGBRegressor(base_score=None, booster=None, callbacks=None,

colsample_bylevel=None, colsample_bynode=None,

colsample_bytree=None, early_stopping_rounds=None,

enable_categorical=False, eval_metric=None, feature_types=None,

gamma=0.40973497757318345, gpu_id=None, grow_policy=None,

importance_type=None, interaction_constraints=None,

learning_rate=0.31952389742711895, max_bin=None,

max_cat_threshold=None, max_cat_to_onehot=None,

max_delta_step=None, max_depth=20, max_leaves=None,

min_child_weight=7, missing=nan, monotone_constraints=None,

n_estimators=101, n_jobs=None, num_parallel_tree=None,

predictor=None, random_state=None, ...)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

XGBRegressor(base_score=None, booster=None, callbacks=None,

colsample_bylevel=None, colsample_bynode=None,

colsample_bytree=None, early_stopping_rounds=None,

enable_categorical=False, eval_metric=None, feature_types=None,

gamma=0.40973497757318345, gpu_id=None, grow_policy=None,

importance_type=None, interaction_constraints=None,

learning_rate=0.31952389742711895, max_bin=None,

max_cat_threshold=None, max_cat_to_onehot=None,

max_delta_step=None, max_depth=20, max_leaves=None,

min_child_weight=7, missing=nan, monotone_constraints=None,

n_estimators=101, n_jobs=None, num_parallel_tree=None,

predictor=None, random_state=None, ...)# =============================================

# Hyper-parameter tuning using Bayesian Optimization

# =============================================

# Optimization objective

def cv_score(parameters):

"""

Define the objective function based on the cross-validation score

Inputs:

parameters: model hyper-parameters to be tuned

Outputs:

cross-validation score

"""

# get the model parameters

parameters = parameters[0]

# define a cross-validation score mode and calculate it

score = cross_val_score(

XGBRegressor(learning_rate=parameters[0],

gamma=parameters[1],

max_depth=int(parameters[2]),

n_estimators=int(parameters[3]),

min_child_weight = parameters[4]),

X_train, y_train, scoring='neg_mean_squared_error').mean()

# remodify a score

score = np.array(score)

return score

# Define the model hyperparameters and the range

# to be tuned

bds = [{'name': 'learning_rate', 'type': 'continuous', 'domain': (0, 1)},

{'name': 'gamma', 'type': 'continuous', 'domain': (0, 5)},

{'name': 'max_depth', 'type': 'discrete', 'domain': (1, 50)},

{'name': 'n_estimators', 'type': 'discrete', 'domain': (1, 300)},

{'name': 'min_child_weight', 'type': 'discrete', 'domain': (1, 10)}]

# Model data:

# Python package: GpyOpt

# f: objective function

# domain: model hyper-parameters boundaries

# model_type: surrogate model -> GP

# acquisition_type: expectation improvement

# acquisition_jitter: a small number added to avoid model instability ->0.05

# exact_feval: if True: it is assumed that cross-validation in Hyper-Parameter-

# space is deterministic

# maximize: optimization type

optimizer = BayesianOptimization(f=cv_score,

domain=bds,

model_type='GP',

acquisition_type ='EI',

acquisition_jitter = 0.05,

exact_feval=True,

maximize=True)

# Start running the model

# Maximum number of iterations is set to be 20,

# considering the number of initial points (default = 5)

# the maximum number of iterations is 25

optimizer.run_optimization(max_iter=20)

# =============================================

# Hyper-parameters value after tuning them using

# Bayesian optimization

# =============================================

hp_tunes_BO = optimizer.x_opt

print("============================================\n")

print("The optimal learning rate is: ", round(hp_tunes_BO[0], 4))

print("============================================\n")

print("The optimal gamma is: ", round(hp_tunes_BO[1], 4))

print("============================================\n")

print("The optimal max_depth is: ", hp_tunes_BO[2])

print("============================================\n")

print("The optimal n_estimators is: ", hp_tunes_BO[3])

print("============================================\n")

print("The optimal min_child_weight is: ", hp_tunes_BO[4])

print("============================================\n")

============================================

The optimal learning rate is: 0.165

============================================

The optimal gamma is: 0.0948

============================================

The optimal max_depth is: 50.0

============================================

The optimal n_estimators is: 300.0

============================================

The optimal min_child_weight is: 1.0

============================================

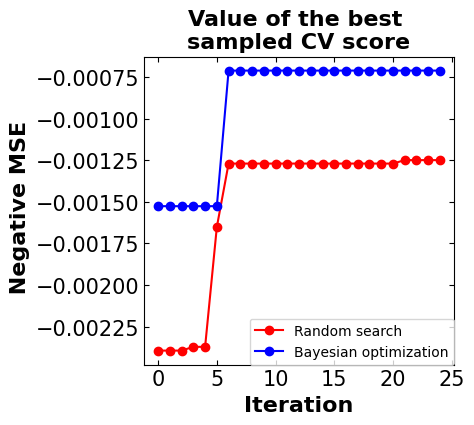

Step 8: Results and discussion#

# =============================================

# The plot of negative mean squared variation

# per iteration considering both algorithms

# =============================================

y_rs = np.maximum.accumulate(rs.cv_results_['mean_test_score'])

y_bo = np.maximum.accumulate(-optimizer.Y[:]).ravel()

# start plotting

fig_compare_tuning = plt.figure(figsize=(4, 4))

# title

plt.title(('Value of the best \n'

'sampled CV score'), fontsize=16, fontweight='bold');

# plot random search results

plt.plot(y_rs, 'ro-', label='Random search')

# plot Bayesian optimization results

plt.plot(y_bo, 'bo-', label='Bayesian optimization')

# define labels attributes

plt.xlabel('Iteration', fontsize=16, fontweight='bold')

plt.ylabel(' Negative MSE', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

plt.legend(fontsize=10, loc='lower right', borderaxespad=0)

plt.show()

print(f'Baseline MSE = {baseline:.5f}')

print(f'Random search MSE = {y_rs[-1]:.5f}')

print(f'Bayesian optimization MSE = {y_bo[-1]:.5f}')

Baseline MSE = -0.00061

Random search MSE = -0.00125

Bayesian optimization MSE = -0.00071

# =============================================

# the models' prediction

# =============================================

# find the predicted values using random search

y_predict_rs = rs.predict(X_test)

# find the predicted values using Bayesian optimization

# In the Bayesian optimization approach we need to reconstruct the model

model_bo = XGBRegressor(learning_rate=optimizer.x_opt[0],

gamma=optimizer.x_opt[1],

max_depth=int(optimizer.x_opt[2]),

n_estimators=int(optimizer.x_opt[3]),

min_child_weight = optimizer.x_opt[4], )

model_bo.fit(X_train, y_train)

y_predict_bo = model_bo.predict(X_test)

# -------------------------------------------------------------------------

# Plot the observation

fig_compare = plt.figure(figsize=(8, 4))

plt.subplot(1, 2, 1)

# title

plt.title(('Randomized Search'), fontsize=16, fontweight='bold')

# plot data predicted values versus actual data

plt.plot(y_test, y_test, 'k', linewidth=3)

plt.scatter(y_predict_rs, y_test, marker = 'o', c = 'b', linewidth=4)

# define labels attributes

plt.xlabel('Y Predicted', fontsize=16, fontweight='bold')

plt.ylabel('Y Real', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

plt.subplot(1, 2, 2)

# title

plt.title(('Bayesian Optimization'), fontsize=16, fontweight='bold')

# plot data predicted values versus actual data

plt.plot(y_test, y_test, 'k', linewidth=3)

plt.scatter(y_predict_bo, y_test, marker = 'o', c = 'b', linewidth=4)

# define labels attributes

plt.xlabel('Y Predicted', fontsize=16, fontweight='bold')

plt.ylabel('Y Real', fontsize=16, fontweight='bold')

# adjust tick sizes

plt.xticks(fontsize=15)

plt.yticks(fontsize=15)

plt.tick_params(direction="in",top=True, right=True)

plt.tight_layout()

plt.show()

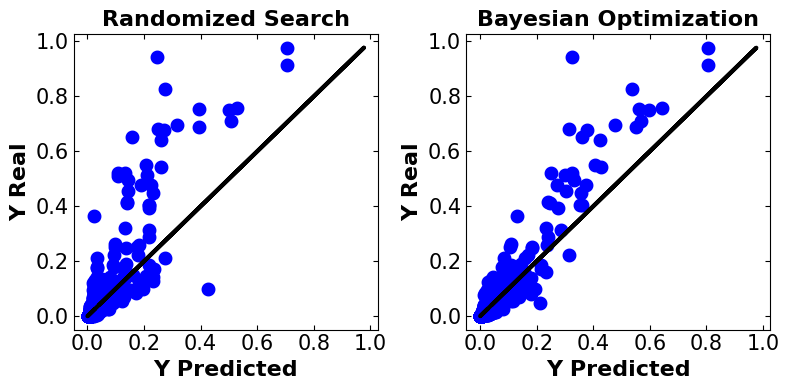

Discussion#

Before starting the discussion here is some information regarding the evaluation metrics.